The global electronics and industrial landscape is undergoing a profound transformation as the limits of traditional silicon-based technologies are reached. Silicon carbide (SiC), a wide-bandgap semiconductor material, has emerged as the definitive successor, offering unparalleled thermal conductivity, high-voltage resistance, and energy efficiency. The shift toward electrification, particularly in the automotive and renewable energy sectors, has positioned SiC as a critical enabler of the next generation of high-performance power systems.

Market Overview and Growth Trajectory

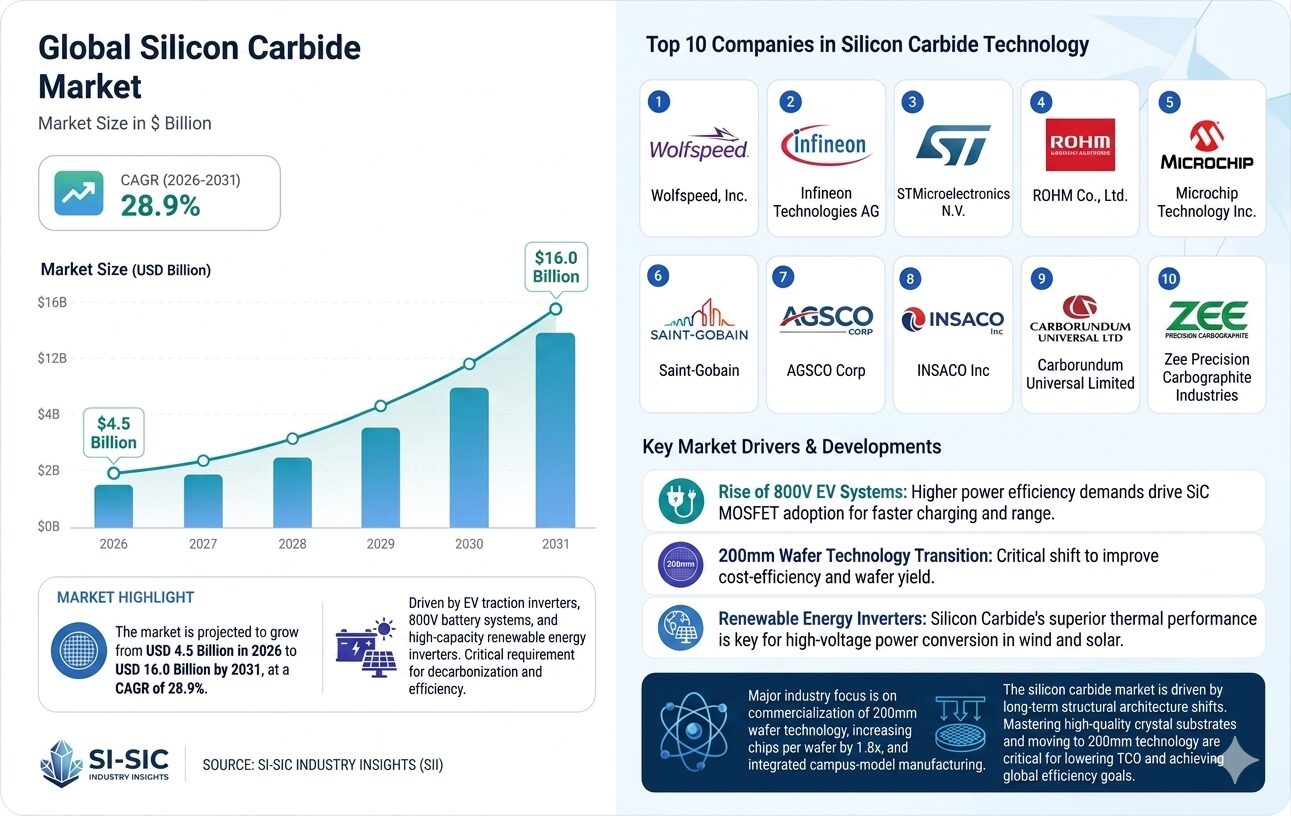

The Silicon Carbide Market is forecast to hit USD 16.0 billion by 2031 from USD 4.5 billion in 2026, at a 28.9% CAGR. This aggressive growth rate is driven by the structural transition in power electronics, where efficiency and power density are the primary metrics of success. Unlike standard silicon, silicon carbide allows for significantly higher switching frequencies and operates reliably at extreme temperatures, which reduces the need for bulky cooling systems and enables more compact, lightweight designs.

Key Market Drivers

1. The Electric Vehicle (EV) Revolution

The automotive sector is the single largest consumer of high-purity silicon carbide. SiC MOSFETs and diodes are becoming the standard for traction inverters, onboard chargers (OBC), and DC/DC converters. By utilizing 800V architectures, automakers can reduce charging times and increase driving range two of the most significant barriers to consumer adoption of EVs.

2. Renewable Energy and Grid Modernization

As the global energy mix shifts toward solar and wind, the demand for efficient power conversion systems has surged. SiC-based inverters are essential for minimizing energy loss during the conversion of DC power from solar panels into AC power for the grid. Furthermore, SiC’s ability to handle high voltages makes it ideal for long-distance HVDC power transmission.

3. 5G Infrastructure and Telecommunications

The deployment of 5G networks requires high-frequency power amplifiers and power supplies that can operate in dense, high-temperature environments. Silicon carbide’s thermal properties ensure that telecom infrastructure remains stable and efficient even under the heavy loads required by modern high-speed data transmission.

Technological Trends and Wafers Transition

The industry is currently witnessing a pivotal shift in manufacturing scale. To improve cost-efficiency and meet the massive volume requirements of the automotive industry, major players are transitioning from 150mm (6-inch) to 200mm (8-inch) wafers.

200mm Adoption: This transition allows for a higher number of dies per wafer, effectively lowering the per-unit cost of SiC devices and making them more competitive with traditional silicon alternatives.

300mm Innovations: Cutting-edge research, such as Wolfspeed’s recent introduction of a 300mm SiC platform, is pushing the boundaries even further, specifically targeting heat dissipation in AI-driven data centers.

Market Segmentation

The market is categorized into several critical segments based on product type and application:

By Product Type:

Black Silicon Carbide: Dominant in industrial applications like refractories, abrasives, and metallurgy where cost-efficiency is prioritized over electrical purity.

Green Silicon Carbide: Higher purity levels make it the preferred choice for precision wafer-polishing and high-performance electronic substrates.

By Application:

Semiconductors: The fastest-growing segment, focused on power discrete devices and modules for energy conversion.

Industrial Ceramics: Used in extreme-temperature equipment, aerospace components, and ballistic armor.

Competitive Landscape

The market is characterized by significant capital expenditure and strategic long-term supply agreements. Major players are investing billions into new fabrication facilities (fabs) to secure their position in the supply chain.

Major players: Wolfspeed, Inc., Microchip Technology Inc., INSACO Inc, Carborundum Universal Limited, Zee Precision Carbographite Industries.

Wolfspeed, Inc.: A pioneer in SiC wafer production and power devices, Wolfspeed is leading the charge in 200mm and 300mm technology.

Microchip Technology Inc.: Focused on providing integrated SiC solutions, including MOSFETs and digital controllers, catering to industrial and automotive reliability.

Carborundum Universal Limited (CUMI): A key player in the material science aspect, providing high-quality SiC grains and powders for both abrasive and refractory applications.

INSACO Inc: Specializes in the precision machining of hard materials like silicon carbide, supporting aerospace and medical applications where tolerances are extreme.

Regional Analysis

The Asia-Pacific region remains the largest market for silicon carbide, supported by China’s dominant position in EV manufacturing and the concentrated semiconductor ecosystem in Taiwan and South Korea. However, North America and Europe are rapidly expanding their domestic capacities through government-backed initiatives like the CHIPS Act and EU State aid, aiming to secure localized supply chains for critical green technologies.

Future Outlook

The trajectory for the Silicon Carbide market is one of rapid maturation. While supply chain volatility and the high cost of raw materials remain challenges, the economies of scale provided by larger wafer formats and increased fab capacity are expected to drive down costs. By 2031, silicon carbide will likely be the foundational material for almost all high-voltage power electronics, cementing its role as a cornerstone of the global energy transition.