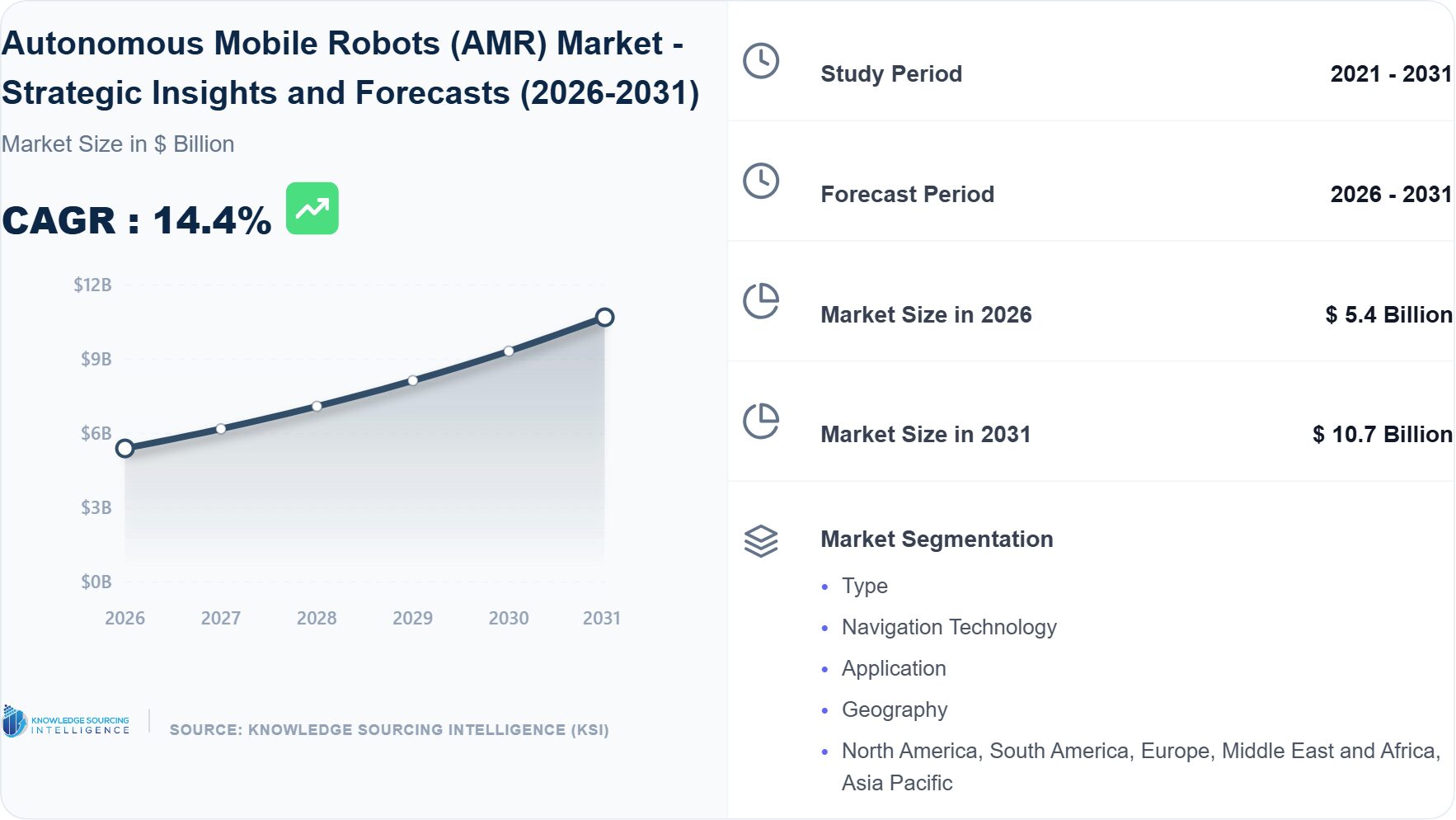

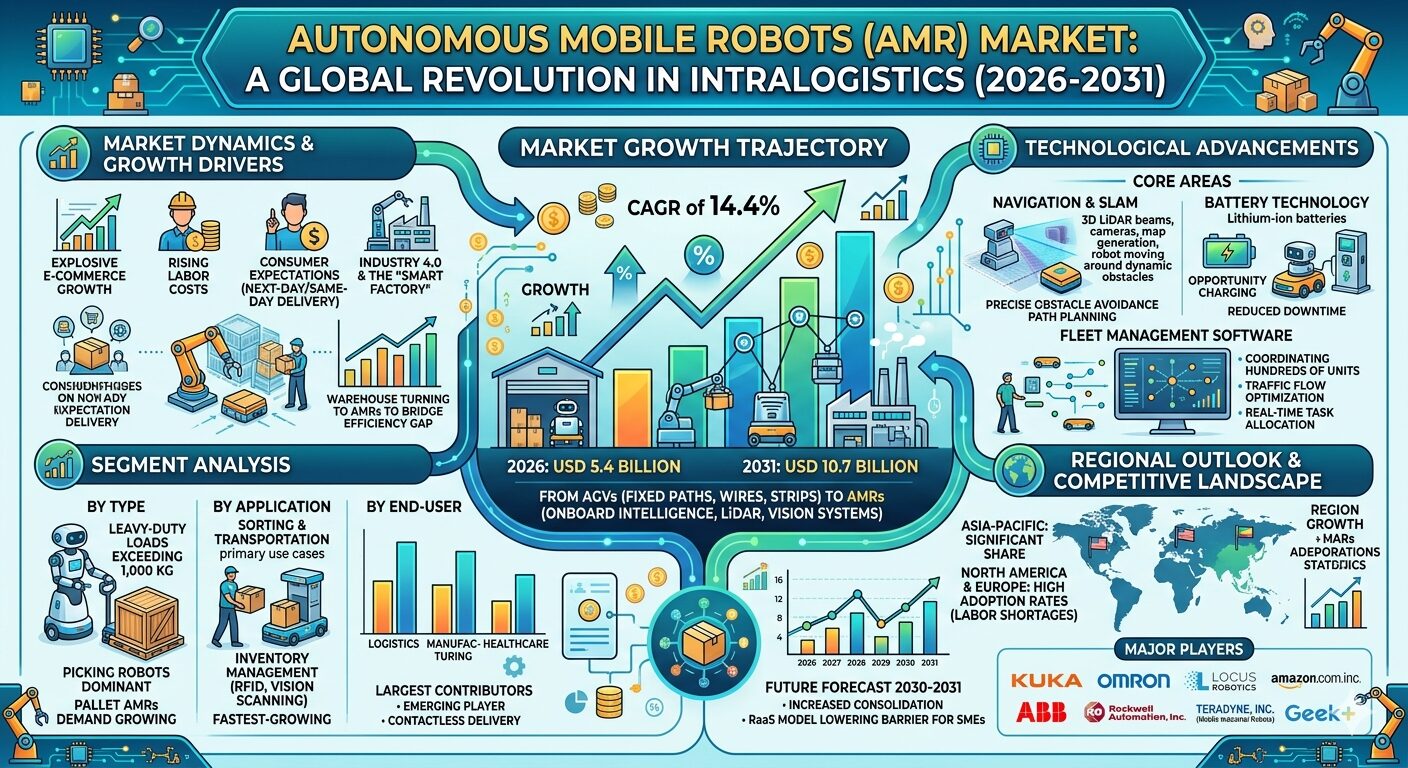

The global landscape of industrial automation is undergoing a seismic shift, moving away from rigid, fixed-path systems toward fluid, intelligent, and decentralized operations. The autonomous mobile robots (AMR) market is set to reach USD 10.7 billion in 2031, growing at a CAGR of 14.4% from USD 5.4 billion in 2026. This rapid expansion highlights the transition from traditional Automated Guided Vehicles (AGVs) to sophisticated AMRs that utilize Simultaneous Localization and Mapping (SLAM) and advanced sensor suites to navigate complex, unstructured environments.

The Evolution of Material Handling

For decades, material handling in warehouses and factories was dominated by manual forklifts or AGVs that required extensive infrastructure—such as magnetic tape or floor-embedded wires—to operate. The modern AMR has shattered these constraints. By integrating LiDAR (Light Detection and Ranging), 3D cameras, and ultrasonic sensors, these robots can interpret their surroundings in real-time, allowing them to dodge obstacles, navigate around human workers, and recalculate paths instantly.

The value proposition of AMRs lies in their “zero-infrastructure” requirement. Unlike legacy systems, an AMR can be deployed in a facility within hours rather than weeks, as it maps the environment digitally during its first run. This agility is particularly vital in the current economic climate, where supply chains must adapt to fluctuating consumer demands and rapid SKU proliferation.

Key Market Growth Drivers

Several macro-economic and technological factors are propelling the AMR market forward:

Labor Scarcity and Rising Costs: Global logistics hubs are facing a chronic shortage of manual labor. AMRs provide a reliable solution for repetitive, “dull, dirty, and dangerous” tasks, allowing human employees to focus on higher-value activities like quality control and strategic planning.

E-commerce Proliferation: The rise of online shopping necessitates faster picking and packing cycles. AMRs, specifically those designed for “goods-to-person” workflows, significantly reduce the walking time for warehouse staff, doubling or tripling productivity.

Advancements in AI and Edge Computing: The integration of Artificial Intelligence allows AMRs to go beyond simple navigation. They can now optimize their own routes based on traffic patterns, predict potential maintenance needs, and communicate with other robots in a collaborative “swarm.”

Segmenting the AMR Landscape

The market is diverse, catering to a wide array of payloads and environments:

Logistics & Warehousing: This remains the largest segment. AMRs are used for sorting, order fulfillment, and transporting heavy pallets.

Manufacturing: In automotive and electronics assembly, AMRs act as flexible conveyor belts, transporting sub-assemblies between work cells without the need for fixed lines.

Healthcare and Hospitality: A burgeoning segment where AMRs are utilized for the sterile transport of medical supplies, linen management in hotels, and even contactless meal delivery.

Regional Market Analysis

The Asia-Pacific region is a primary engine of growth, bolstered by massive investments in smart manufacturing in China, Japan, and South Korea. India is also emerging as a significant market as its domestic logistics sector undergoes digital transformation. In North America and Europe, the focus is on high-end technological integration, with a strong emphasis on safety standards and collaborative robotics.

Strategic Competitive Environment

The competitive landscape is characterized by intense innovation and strategic partnerships between software developers and hardware manufacturers. Companies are increasingly focusing on “interoperability”—ensuring that a fleet of robots from different vendors can be managed through a single software interface.

Major players in the industry include:

Teradyne (Mobile Industrial Robots)

Zebra Technologies (Fetch Robotics)

ABB (ASTI Mobile Robotics)

Honeywell International Inc.

Fetch Robotics, Inc.

BlueBotics

Future Outlook and Projections

As we approach the turn of the decade, the convergence of 5G connectivity and AMRs will unlock even greater potential. 5G’s low latency will enable more processing to happen in the cloud, allowing for lighter, more energy-efficient robots that can stay on the floor for longer durations. Furthermore, the “Robots-as-a-Service” (RaaS) business model is expected to gain significant traction, moving the investment from a Capital Expenditure (CAPEX) to an Operational Expenditure (OPEX), thereby making advanced automation accessible to small-scale enterprises.

The autonomous mobile robots market is forecast to hit USD 10.7 billion by 2031 from USD 5.4 billion in 2026, at 14.4% CAGR. Major players: Teradyne, Zebra Technologies, and ABB. This growth underscores a future where autonomous movement is the backbone of the global economy, driving efficiency and safety to unprecedented levels.