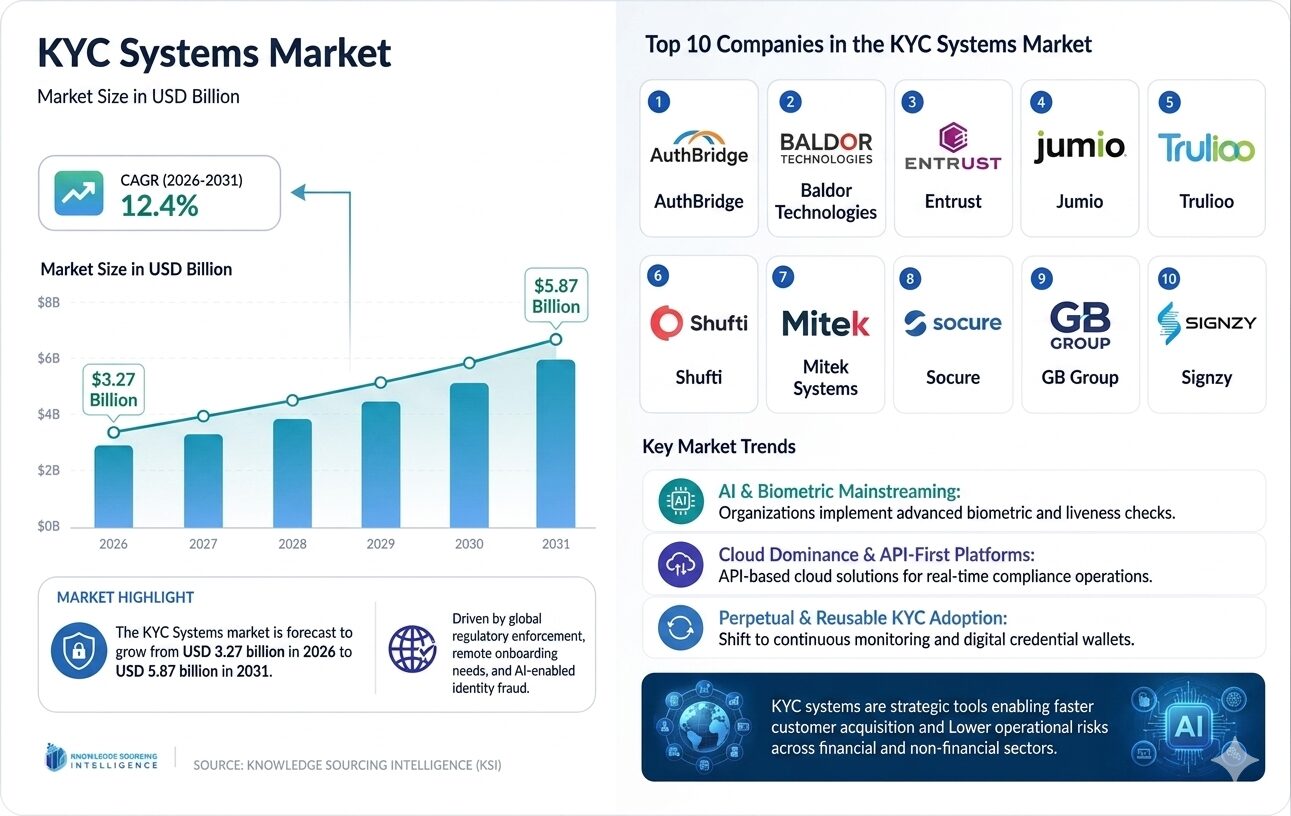

The KYC Systems market is forecast to grow at a CAGR of 12.4%, reaching USD 5.87 billion in 2031 from USD 3.27 billion in 2026, supported by a structural shift in how organizations perceive identity, risk, and customer onboarding across industries.

The U.S. Market Isn’t Growing Fast—It’s Growing Relentlessly

Growth in the U.S. KYC systems market doesn’t come in bursts. It accumulates. Quietly, persistently, and often reactively.

That’s partly because compliance isn’t optional. It tightens incrementally—through updated AML expectations, rising suspicious activity reports, and more aggressive enforcement patterns. The result is a market that doesn’t rely on hype cycles. It expands because it has to.

Recent estimates suggest the U.S. KYC software segment alone is already in the multi-billion-dollar range and continuing to climb steadily, driven by regulatory pressure and fraud risks rather than discretionary IT spending . At the same time, North America accounts for a significant portion of global adoption, reflecting how deeply compliance technology is embedded into financial infrastructure .

But here’s the nuance: growth isn’t just about more institutions buying KYC tools. It’s about existing users replacing what they already have.

Replacement, Not Adoption, Is the Real Market Driver

The popular assumption is that KYC growth is driven by new adopters—fintech startups, digital lenders, or crypto platforms. That’s only part of the story.

In the U.S., the bigger driver is replacement.

Banks and financial institutions are actively dismantling legacy KYC frameworks built a decade ago. These systems were designed for static verification—collect documents, run checks, archive results. That model no longer works.

Today’s environment demands:

Real-time identity validation

Continuous monitoring

Cross-channel risk visibility

Legacy systems struggle with all three.

More than 70% of institutions in developed markets are already transitioning toward automated and digital-first KYC processes . That statistic hints at a deeper truth: KYC transformation is less about innovation and more about catching up.

The Hidden Cost Problem Nobody Talks About

KYC discussions tend to focus on compliance risk, but operational cost is just as important—and often underestimated.

Inside most U.S. financial institutions, KYC is still labor-intensive. Even with automation, edge cases pile up:

Incomplete documentation

False positives

Manual reviews for ambiguous identities

Industry conversations—particularly among fintech operators—suggest that manual “case handling” remains one of the biggest bottlenecks in scaling KYC operations. Teams often discover that automation handles only the straightforward majority, while a stubborn minority of cases consumes disproportionate resources.

This creates a paradox. Automation reduces workload overall but exposes inefficiencies more clearly. Institutions then invest further—not just in verification tools, but in workflow orchestration, case management, and audit trails.

The result is a layered KYC stack, not a single solution.

U.S. Regulatory Pressure: Fragmentation Drives Sophistication

If there’s one factor that consistently shapes the U.S. KYC market, it’s regulatory fragmentation.

Unlike regions with centralized frameworks, the U.S. system distributes oversight across multiple entities. This leads to:

Overlapping requirements

Slightly different interpretations of the same rule

Continuous updates rather than periodic overhauls

From a technology perspective, this forces flexibility.

Institutions aren’t just buying KYC systems—they’re buying adaptability. Solutions must accommodate evolving rules tied to the Bank Secrecy Act, the Patriot Act, and FinCEN guidance, all of which require ongoing monitoring and reporting capabilities .

Interestingly, this fragmentation has an unintended upside. It encourages innovation. Vendors compete not just on features, but on how quickly they can adapt workflows to regulatory nuance.

Digital Banking Changed the Rules—And the Timeline

There was a time when KYC processes could take days. Customers expected it.

That expectation is gone.

With over 70% of U.S. adults using online banking, digital onboarding has become the default, not the exception . This compresses the KYC timeline dramatically.

Institutions now face a delicate balancing act:

Move too slowly → lose customers

Move too quickly → increase fraud risk

KYC systems sit directly in that tension.

Modern platforms aim to resolve it through:

Instant document verification

Biometric authentication

Risk-based onboarding (different checks for different users)

But even here, trade-offs persist. Increasing verification rigor often reduces conversion rates. Relaxing controls can expose vulnerabilities.

There’s no perfect equilibrium—only better calibration.

U.S. Companies Driving Practical Innovation

Experian (Costa Mesa, California)

Experian’s strength lies in identity data aggregation. Its KYC capabilities draw from credit histories, behavioral data, and alternative datasets, creating a multi-dimensional view of identity.

What’s notable is its predictive approach. Instead of verifying identity in isolation, Experian evaluates the likelihood of legitimacy based on historical patterns. This shifts KYC from a binary process to a probabilistic one.

Alloy (New York City, New York)

Alloy operates more like an orchestration layer than a traditional KYC provider. It connects multiple data sources, verification tools, and decision engines into a unified workflow.

This approach reflects a growing industry realization: no single vendor solves KYC entirely. The value lies in how components work together.

Alloy’s rise suggests that integration—long overlooked—is becoming a primary battleground.

Plaid (San Francisco, California)

While primarily known for financial data connectivity, Plaid has moved into identity verification through transaction-based insights.

This introduces an interesting dimension: behavioral verification. Instead of relying solely on documents, Plaid analyzes financial activity patterns to validate identity.

It’s not a replacement for traditional KYC, but it adds another layer—one that’s harder to fake.

Jumio (Sunnyvale, California)

Jumio focuses heavily on biometric verification and AI-driven document analysis. Its systems are widely used in industries where fraud risk is high and onboarding must remain frictionless.

The company’s emphasis on automation highlights a broader trend: reducing reliance on manual review while maintaining auditability.

The Real Battlefield: Orchestration vs. Accuracy

There’s an ongoing debate within the industry that rarely surfaces in formal reports: what matters more—accuracy or orchestration?

Accuracy refers to how well a system verifies identity and detects fraud. Orchestration refers to how well different components work together.

Historically, vendors competed on accuracy. Today, orchestration is catching up.

Why? Because even highly accurate systems create friction if they don’t integrate smoothly into broader workflows. A fragmented KYC stack leads to:

Delayed onboarding

Inconsistent risk scoring

Operational inefficiencies

This is why many U.S. institutions are investing in orchestration platforms. Not because individual tools are inadequate, but because coordination between them is.

Emerging Patterns That Will Shape the Next Phase

Continuous Identity, Not One-Time Verification

KYC is evolving into an ongoing process. Systems will increasingly monitor behavior over time rather than relying solely on initial verification.

Risk-Based Personalization

Not all customers require the same level of scrutiny. Future systems will dynamically adjust verification intensity based on risk profiles.

AI—But With Constraints

AI adoption is accelerating, but regulatory expectations around transparency limit how it can be used. Explainability is becoming as important as accuracy.

Expansion Beyond Finance

KYC is moving into sectors like online marketplaces, healthcare platforms, and digital services. Identity verification is becoming a universal requirement, not a financial one.

A Market That Rewards Realism Over Ambition

The KYC systems market in the United States isn’t driven by bold visions. It’s shaped by constraints—regulatory, operational, and technological.

That’s what makes it interesting.

Growth to USD 5.87 billion by 2031 reflects not just increasing demand, but increasing complexity. Institutions aren’t looking for perfect solutions. They’re looking for workable ones—systems that reduce friction, manage risk, and adapt over time.

And that may be the defining characteristic of this market: progress measured not in breakthroughs, but in incremental improvements that, collectively, redefine how trust is built.